Schedule a talk with one of our advisors to learn more about Summitry and how we can help you get a foothold on your financial life.

Team

Insights

Pages

- Let's Talk

- Phone / Directions

5 Actions to Take in a Bear Market

Adam Govani, CFP®

Sep 9, 2022

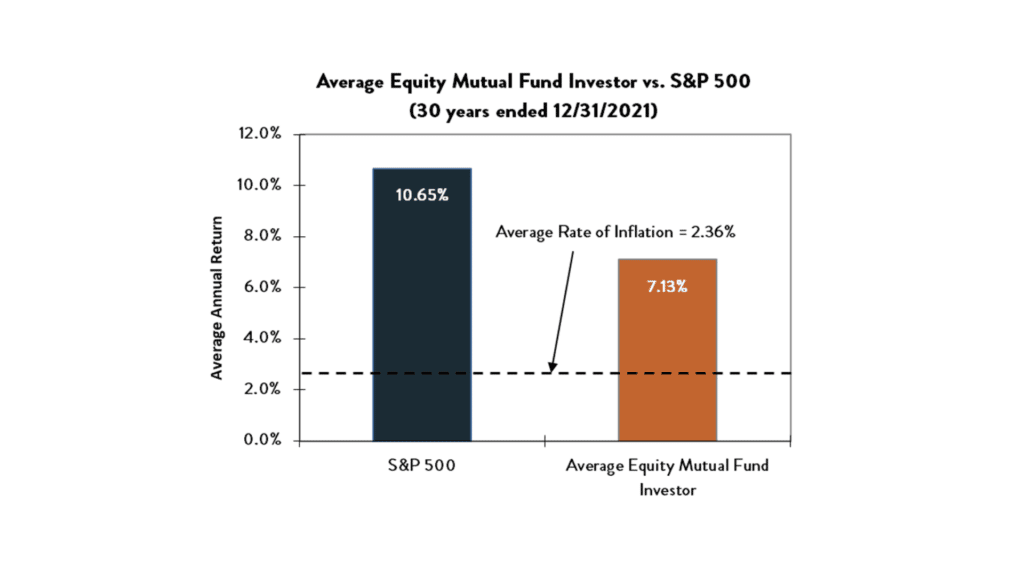

During periods of volatility, sometimes the most difficult thing to do is nothing. Our brains are wired for action and watching a decline in your net worth can drive investors to take actions detrimental to their long-term success, such as market-timing and performance-chasing. The oft-cited Quantitative Analysis of Investor Behavior (QAIB) from Dalbar shows that this trend persisted throughout 2021. The average equity fund investor trailed the S&P 500 by ~10%; a massive gap and the third largest since 1985, when the QAIB was first released.

Source: Dalbar

Source: Dalbar

Moreover, this gap jumped 10x from 2020, a significantly more volatile year. In essence, investors seemed to have weathered the 2020 storm only to fall behind in the relatively benign market of 2021. Clearly investors are deviating from their strategy in ways that have set them far behind a plain vanilla index.

What this highlights is that the average equity fund investor would have been better served by doing nothing. However, embracing our human need for doing something in a time of uncertainty, we would offer the following as more prudent when looking to protect and grow wealth for the long-term.

Review Your Expenses

Many of our clients are in the fortunate situation that they do not have a defined budget. In this case, reviewing expenses is less about making ends meet and more about feeling in control of your finances. In good times, we tend to spend without much constraint. Chances are you have at least one subscription that you rarely use, or perhaps another recurring expense that provides little utility. Reducing these expenses may not make or break your financial plan, but it provides a sense of control when we feel unsettled.

Respond Rather than React

When stressed by external events, we tend to become reactive. A reactive investor is swayed by every move in the market and guided by a constant stream of economic data. A responsive investor, in contrast, can reflect on their gut reactions and let it guide an open dialogue. If you find yourself feeling the impulse to change your asset allocation every few months, you are almost certainly reacting. Instead of focusing on external events (to which we feel a desire to act upon), a responsive investor understands the role the portfolio plays in their financial plan. Your advisor can be your partner in this dialogue and help you fashion a thoughtful response.

Change, Slowly

Bull markets can sometimes hide a declining tolerance for risk, and bear markets may reveal asset allocations that are more aggressive than feels comfortable. If this describes your frame of mind, speak to your advisor about risk and asset allocation in the context of your long-term financial plan. Just because a portfolio has fallen in value does not preclude making a change if change is appropriate; many of our clients become more risk averse as they approach retirement. Well-discussed and prudent changes are different than chasing the hottest investment fad. Making incremental changes can satisfy our desire to respond (not react) in a responsible manner.

Check your Cash

There are many reasons an investor may hold cash (or equivalents, such as money market funds): these are generally strategic (as part of an asset allocation) or tactical (used to meet a specific planning need). In the last few years, interest rates have been pegged near zero. Consequently, there was little impetus to seek out higher-yielding alternatives for old-fashioned bank deposits. Now that the Federal Reserve has raised short-term interest rates, investors can receive substantially higher yields on low-risk alternatives, such as certificates of deposit or Treasury bills. While these assets are not risk-free, they provide FDIC insurance and the full faith and credit of the US government, respectively. Yields on money market funds have also risen substantially above levels that are generally available in bank savings accounts. Even more mundane options, like a high-yield savings account, can be an excellent parking spot for cash reserves not needed in the next three to six months.

Review your Taxes

This would not be a Summitry blog post if we did not discuss taxes! If you are basing your 2022 tax projections on 2021 numbers, this is a great time to review and potentially, revise. For example, many of our clients have variable compensation, such as company equity. As equity prices have fallen, this is a perfect time to reassess whether you might be overpaying your estimated taxes based on 2021 figures. A down market also creates opportunities for tax-loss harvesting. While not appropriate for everyone, those in a high-income tax bracket or with significant capital gains, such as the sale of appreciated equities or real estate, may benefit substantially from reducing their capital gains by offsetting with capital losses.

Watch our webinar “Bear Market Behavior: How to Confidently Weather the Storm” on-demand where we discuss these strategies and more and take questions from participants.

Weathering a bear market is not as simple as doing nothing of course, but it’s also critical to align actions with long-term goals rather than in reaction to mercurial markets, particularly in times of uncertainty. The result for investors is greater control, increased security, much-needed comfort, and more confidence in achieving goals in the months and years ahead.

If you aren’t currently a Summitry client, contact us today to speak to an advisor about your financial future.

This article is for informational purposes only; it does not constitute investment advice nor should it suggest that any particular strategy is suitable for any specific person. The S&P 500 is an index. An index is a hypothetical portfolio of securities representing a particular market or market segment used as an indicator of the change in the securities market. Indexes are unmanaged, do not incur fees and expenses and cannot be invested in directly.

GET THE NEXT SUMMITRY POST IN YOUR INBOX:

MORE INSIGHTS AND RESOURCES

Let's talk

Schedule a talk with one of our advisors to learn more about Summitry and how we can help you chart a path for your financial future.

Alex Katz

Chief Growth Officer