Schedule a talk with one of our advisors to learn more about Summitry and how we can help you get a foothold on your financial life. For career opportunities please visit careers at Summitry.

Team

Insights

Pages

- Let's Talk

- Phone / Directions

Summitry Select

1/6/2026

Summitry Select Portfolio Update – Q4 2025

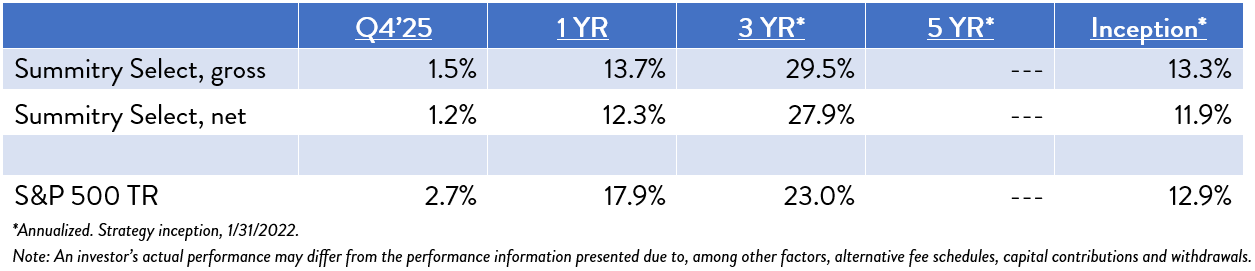

During the fourth quarter of 2025, the Summitry Select composite increased +1.5% (+1.2%, net). The Composite has returned +29.5% (+27.9%, net) annualized over the past 3 years and +13.3% (+11.9%, net) annualized since inception.

As we approach the fourth anniversary of Summitry Select at the end of this month, we think it is worthwhile to reflect on the market environments we have navigated together over the past four years. We believe this period has served as a rigorous proving ground, validating the resilience of our strategy across a wide variety of economic and market conditions.

Our journey began in 2022 during a difficult bear market, a period defined by inflation and rapidly rising interest rates that punished valuations for the businesses we favor. While other investors seemed to discard high-growth quality businesses indiscriminately, we held firm to our conviction that owning a concentrated portfolio of companies with durable economic moats would ultimately be rewarded.

However, we have never been afraid to part ways with positions when the math no longer made sense to us, or our thesis became broken. We sold Disney in early 2024 when the fog of uncertainty around the profitability of streaming and sports rights became too thick. Later that year, we exited CarMax when it became clear to us that new entrants like Carvana had disrupted the used car market, eroding CarMax’s competitive advantage. We even sold Netflix, one of our biggest winners, because the share price had outrun our estimate of the stock’s intrinsic value.

We spent much of 2025 navigating new Trump administration’s trade policies, which sent markets into a tailspin in April. We did not panic. Instead, we relied on the flexibility of our mandate. We re-underwrote every position in the portfolio to stress-test against trade war scenarios and deployed a portion of our cash balance to improve the expected return of our portfolio.

Through each of these environments, our philosophy has remained constant: we operate as business owners, we seek companies offering essential products and services, and we remain disciplined on valuation.

Investment Performance

Our best performers during the quarter were GOOGL (+28.8%), ULTA (+10.7%), and TSM (+8.8%).

- Earlier in 2025, we decided to trim our Alphabet (GOOGL) position as we balanced the potential impact of increased competition from OpenAI and ChatGPT against Google’s competitive advantages and valuation. While we recognized that new competitors were making inroads, we maintained our belief that Google’s AI model capabilities compared favorably and that the company was making the right strategic moves to defend its core Search business. Recent results support our decision to retain a significant holding.

- Ulta Beauty (ULTA) shares rallied as the company continued to emerge from a period of heightened competition. As we noted in our last letter, we believed the competitive intensity from Sephora’s expansion into Kohl’s locations would subside as that rollout completed, and this thesis appears to be playing out. Under the leadership of CEO Kecia Steelman, Ulta has also improved store operations and merchandising. We continue to view the beauty category as particularly resilient to broader economic pressures, and Ulta’s unique one-stop shop model remains a powerful differentiator within the category.

- TSMC (TSM) continues to benefit from insatiable global demand for high-performance computing. As the essential foundry for the AI revolution, TSMC is capturing significant value from the staggering capital investments being made by hyperscalers. Despite concerns about potential tariffs on Taiwanese exports and semiconductor export controls, we believe TSMC’s monopoly at the leading edge provides it with sufficient pricing power to pass on higher costs to customers, protecting its attractive margins and returns on invested capital.

Our worst performers during the quarter were NTDOY (-21.8%), ZBRA (-18.3%), and META (-10.1%).

- Nintendo (NTDOY) gave back much of its gains from earlier in the year. After a successful launch of the Switch 2 console, which we anticipated would unlock significant pent-up demand from the company’s massive installed base, the stock has cooled due to concerns about memory chip shortages. However, we view these concerns as a temporary headwind and remain confident in Nintendo’s unique strategy of leveraging its portfolio of iconic characters to drive recurring revenue and high-margin software sales.

- Zebra Technologies (ZBRA) was negatively impacted by renewed uncertainty surrounding global trade. As we have seen previously, Zebra’s customers in the retail and logistics sectors are sensitive to economic uncertainty and often pause capital budgets when tariff outlooks are unclear. While Zebra has diversified its supply chain to mitigate these risks, the stock remains volatile. However, we continue to believe that Zebra provides mission-critical tools that customers cannot delay purchasing indefinitely.

- We continue to believe Meta Platforms (META) has opportunities to both increase user engagement and drive better monetization from advertisers. However, the rapid adoption of generative AI has created uncertainty about the returns we can expect on the company’s data center investments. With the shares near all-time highs in Q3, we determined that our forecast returns warranted a smaller position. Subsequently, Meta shares faced pressure in Q4 as investors shifted focus from the continued rapid revenue growth at Meta’s core properties to the rising cost of AI investments.

Concluding Thoughts

As we look ahead, we remain grounded in the principles that have guided this portfolio since inception. While we are not afraid to make changes when our thesis is impaired, we are also equally willing to hold firm through volatility when our research suggests our thesis remains valid.

We enter the new year with a sizeable cash balance. In an environment characterized by a fluid geopolitical landscape and rapid technological disruption, this optionality could prove to be an asset. Cash reserves allow us to quickly take advantage of new opportunities without selling existing positions, as we continue to hunt for opportunities to improve the expected return of our portfolio without lowering the quality of our holdings.

As always, thank you for placing your trust in us to search for those opportunities on your behalf. Please do not hesitate to reach out with any questions.

Sincerely,

The Summitry Select Team

Note: This commentary reflects the opinions of Summitry, LLC and is for informational purposes only. Nothing herein constitutes investment advice or any recommendation that any particular strategy or security is suitable for any specific person. Past performance does not guarantee future returns. Investing involves risk and possible loss of principal capital. An index is a hypothetical portfolio of securities representing a particular market or market segment used as an indicator of the change in the securities market. Indexes are unmanaged, do not incur fees and expenses and cannot be invested in directly. The securities identified and described do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Summitry Select Update Archives