Schedule a talk with one of our advisors to learn more about Summitry and how we can help you get a foothold on your financial life. For career opportunities please visit careers at Summitry.

Team

Insights

Pages

- Let's Talk

- Phone / Directions

Summitry Select

7/7/2026

Summitry Select Portfolio Update – Q2 2026

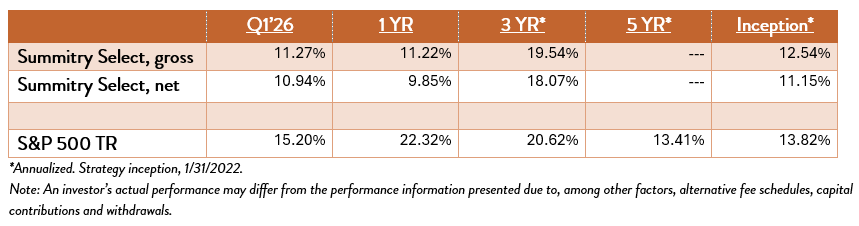

During the second quarter of 2026, the Summitry Select Composite increased 11.27% (10.94%, net). All but three of our positions, Meta, Nintendo, and Ulta, appreciated, and most were up by double digit percentages. The Composite has returned +19.54% (+18.07%, net) annualized over the past 3 years and +12.54% (+11.15%, net) annualized since inception.

Investors had no shortage of concerns to contemplate during the first half of the year: war, an election year, inflation, a sluggish housing market, and a strained consumer. However, by far the most important market theme over the past six months has been the continued development and adoption of AI by consumers and businesses, along with the ongoing investments in compute infrastructure required to support that adoption.

This theme produced sharp divergence in stock performance between companies perceived to be AI winners and those viewed as losers. Former market darlings, particularly software companies, declined by as much as 40% in some cases. Meanwhile, semiconductor companies — viewed by investors as the “picks and shovels” of the AI revolution — became the new market favorites, delivering extraordinary returns and, in some cases, compressing what would normally be decades’ worth of gains into a single quarter.

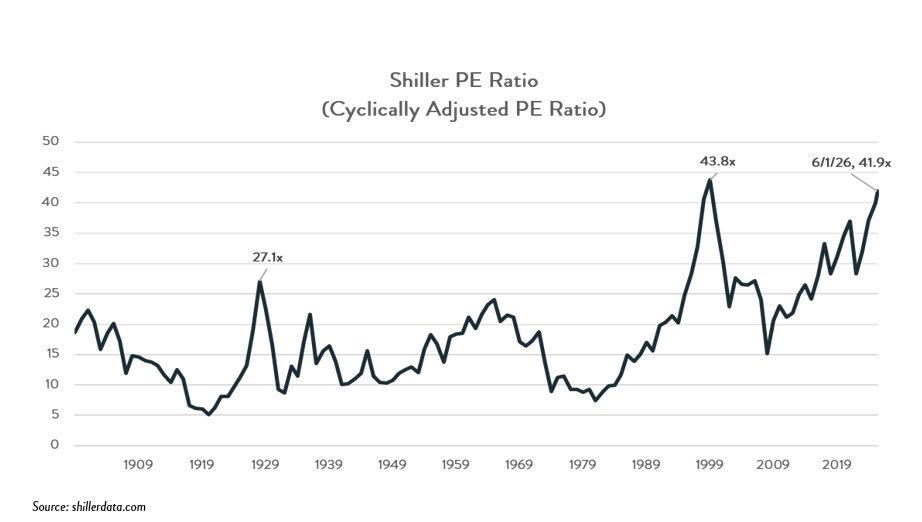

The move has been supported by strong revenue and earnings growth, but this is only part of the story. Valuations for many semiconductor stocks have expanded to historic levels, implying investors expect strong earnings growth to persist well into the future. In some cases, price-to-earning ratios have expanded to roughly 4x their 10-year historical averages, driving the overall benchmark to levels not seen since the internet bubble.

Markets tend to operate like an imperfect pendulum, constantly swinging between greed and fear. When prices move toward one of those extremes, both risks and opportunities rise, and investors need to be especially careful about how they conduct themselves. The feeling of missing out on a massive upswing is never comfortable, but when returns begin to look more like lottery-ticket outcomes, we prefer to focus on capital preservation and opportunities that do not require us to be lucky. Rather than chasing the current hot thing, we continue to pick our spots carefully, balancing business quality, durability of earnings, and valuation.

Q1 Portfolio Activity

During the second quarter, we added to our positions in Zebra Technologies (ZBRA) and Nintendo, trimmed our position in Taiwan Semiconductor Manufacturing Company (TSM), and purchased a new position in Uber Technologies (UBER).

Zebra is a leader in mobile computers and industrial printers. The business is cyclical, but it benefits from long-term trends in automation, reshoring, digital commerce, and increasingly complex supply chains. Zebra boomed during the pandemic, then suffered a cyclical decline, and has been on a recovery path since. Long-term replacement demand is the largest driver of revenue growth, and that demand has accelerated in recent quarters. Honeywell, Zebra’s largest competitor, sold its business, and Zebra has been taking share. We think Zebra may have an opportunity to take additional share as that competitor works through integration.

Nintendo remains out of favor, mostly because investors are worried that memory chip shortages will hurt sales. One of the biggest beneficiaries of the AI infrastructure build has been memory chip companies, but the other side of that strength is that companies like Nintendo may have to pay more for memory. We think Nintendo has sufficient memory supply and that this issue should not have a meaningful long-term impact on margins or profits. With the stock appearing extremely discounted to us, we decided to add to the position.

TSMC continues to stand tall at the heart of the semiconductor ecosystem due to its monopoly position in manufacturing cutting-edge chips. The business has been booming thanks to insatiable demand for AI silicon that only TSMC can provide at quality, costs, and scale acceptable to customers. However, the stock participated fully in the AI boom and has roughly doubled over the past year, so we decided to reduce the position size.

Uber needs little introduction, but the scale of its business may still surprise many investors. In the first quarter alone, Uber generated $54 billion in bookings. Its drivers completed 3.6 billion trips, and nearly 200 million consumers used the platform.

Uber has two powerful profit engines: Mobility and Delivery. Both continue to grow rapidly. The brand is so dominant in ridesharing that “Uber” has become a verb, a testament to its strength and consumer loyalty. We also believe there is meaningful runway for growth in new geographies and adjacent categories, including travel.

Delivery has become Uber’s fastest-growing profit stream. It is a three-sided network that creates value for restaurants, couriers, and consumers. The business continues to expand into groceries and suburban markets. Together, Mobility and Delivery reinforce one another, creating a stronger platform than either business could achieve alone.

Our investment process begins with the moat, and we believe Uber’s competitive advantage is not only wide but widening. It rests on three pillars. First, global scale. Uber is the leading on-demand platform across mobility, delivery, freight, and travel in more than 70 countries. Second, network effects. Millions of consumers and drivers reinforce one another, creating density that competitors struggle to match. Third, customer loyalty. Uber One increases engagement across the platform and positions Uber to become a broader consumer marketplace over time.

We also see several avenues for future growth. Greater adoption of Uber One increases retention and spending. Advertising is emerging as a high-margin revenue stream. At the same time, operating leverage is allowing earnings and free cash flow to grow faster than revenue.

We are equally impressed by the management team. Under CEO Dara Khosrowshahi, Uber has reached GAAP profitability, generates substantial free cash flow, and has begun returning capital to shareholders through share repurchases.

So why is the opportunity available today? We believe the market remains overly concerned that autonomous vehicles will disrupt Uber’s ridesharing business. We see the opposite. Autonomous vehicles still require demand aggregation and network liquidity, areas where Uber has a significant competitive advantage. We also do not expect the market to become winner-take-all.

Early evidence from San Francisco supports this view. As autonomous vehicles have expanded, Uber has continued to grow. The data suggests autonomy is increasing the size of the transportation market rather than simply shifting share among existing providers.

Uber is also positioning itself as the demand platform for autonomous vehicles. The company is already partnering with leading autonomous vehicle developers and integrating their fleets into its network.

In our view, the market is underestimating Uber’s long-term earnings power. The shares trade at a meaningful discount to our estimate of intrinsic value, creating what we believe is an attractive opportunity.

Investment Performance

Our best performers during the quarter were Taiwan Semiconductor Manufacturing Company (TSM), Alphabet (GOOGL), and Zebra Technologies (ZBRA).

- TSMC gained 39.29% during the quarter as the business continues to demonstrate the dominance of its hard-earned monopoly at the leading edge of semiconductor manufacturing. Demand for AI accelerators remained insatiable and led to upwardly revising its growth forecasts for these products through 2029. We believe TSMC’s central position in the AI revolution will continue to drive its results in the foreseeable future.

- Alphabet gained 28.91% during the quarter. We believe the strength reflects growing investor confidence in the durability of Google’s Search franchise, continued strong demand for Google Cloud, and the company’s improving position in foundational large language models. Although AI is increasing the capital intensity of the business, it is also reinforcing Alphabet’s competitive advantages. The company’s massive global compute infrastructure places it among a small group of businesses with the scale and technical capabilities to power the next generation of AI, further strengthening its moat.

- Zebra shares increased +26.24% during the quarter as the business continued to move along its post-pandemic recovery path. Long-term replacement demand, the largest driver of revenue growth, has accelerated in recent quarters. We also believe Zebra may benefit as Honeywell’s divested business moves through integration, potentially creating an opportunity for Zebra to gain additional share.

Our worst performers during the quarter were Nintendo (NTDOY), ULTA Beauty (ULTA), and Microsoft (MSFT).

- Nintendo declined -24.20% during the quarter as investors worried that memory chip shortages could hurt sales. We view this as a manageable issue. We think Nintendo has sufficient memory supply, and we do not believe higher memory costs should have a meaningful long-term impact on margins or profits. With the shares appearing extremely discounted to us, we added to the position during the quarter.

- Ulta declined 10.04% during the quarter, despite delivering one of the strongest operating performances in our portfolio. Under the leadership of its new CEO, Ulta reported comparable sales growth of 5.3%, well above management’s full-year guidance. Management continues to execute well on several strategic initiatives, and we see no evidence of competitive pressure. At current valuation levels, we believe the shares remain attractive. Management appears to agree, as the company continues to repurchase shares aggressively at what we believe are compelling prices.

- Microsoft was among our weakest performers despite delivering a positive absolute return of 3.31%. The shares were pressured by concerns over heavy AI-related capital spending and the possibility that generative AI could disrupt Microsoft Office’s traditional per-seat SaaS model. We remain optimistic. AI adoption continues to accelerate, with paid Microsoft 365 Copilot seats increasing 160% year over year to 15 million as of January 2026. Meanwhile, Azure continues to grow more than 35% annually, allowing Microsoft to capture a significant share of the compute spending driving the AI revolution.

Concluding Thoughts

In periods like this, it is important to remember not only what we are trying to do, but also what we are not trying to do. We are not in the business of predicting short-term market turns. We are not trying to find the next fad or ride the next short-term market theme. It is easy to get caught up in the frenzy, buy into compelling stories about the future, and roll the dice on risky businesses offered at expensive prices.

In times like these, we double down on business quality, sustainable growth and earnings power, and valuation discipline. Our cash position gives us optionality to hunt for new opportunities to improve the expected return of the portfolio without compromising on the durability of the moats we own.

As always, thank you for placing your trust in us to search for those opportunities on your behalf. Please do not hesitate to reach out with any questions.

Sincerely,

The Summitry Select Team

Note: This commentary reflects the opinions of Summitry, LLC and is for informational purposes only. Nothing herein constitutes investment advice or any recommendation that any particular strategy or security is suitable for any specific person. Past performance does not guarantee future returns. Investing involves risk and possible loss of principal capital. An index is a hypothetical portfolio of securities representing a particular market or market segment used as an indicator of the change in the securities market. Indexes are unmanaged, do not incur fees and expenses and cannot be invested in directly. The securities identified and described do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable. Forward-looking statements are based on current expectations and assumptions and are subject to risks and uncertainties; actual results may differ materially.