Schedule a talk with one of our advisors to learn more about Summitry and how we can help you get a foothold on your financial life. For career opportunities please visit careers at Summitry.

Key Takeaways

- California safe harbor rules are stricter and more front-loaded than the federal rules.

- Avoiding underpayment penalties depends on when you pay, not just how much you pay by year-end.

- California’s standard payment schedule is roughly 30% by April, 70% by June, and 100% by January.

- Equity compensation can make safe harbor harder to meet because income often arrives in large spikes.

- Withholding alone may not cover your California tax liability.

California’s strict and front‑loaded safe harbor rules often catch residents off guard and make them vulnerable to underpayment penalties. Income that is uneven, seasonal, or difficult to predict, such as bonuses, business income, large capital gains, or equity compensation, can make those penalties difficult to avoid without detailed planning.

Underpayment Penalties and Safe Harbor Rules

What is an underpayment (estimated tax) penalty?

An underpayment penalty is essentially interest charged when you don’t pay enough tax early enough during the year. California expects you to pay tax as income is earned, not just when you file your return.

This is different from:

- A late payment penalty, which applies if tax is still unpaid after the filing deadline.

- A late filing penalty, which applies if you file the return itself late.

You may owe no late payment or filing penalties, yet still face an underpayment penalty.

What is a “safe harbor” rule?

A safe harbor is a set of dollar and timing tests. If you meet them, you generally avoid underpayment penalties, even if you still owe additional tax when you file.

Safe harbor does not reduce the tax you owe. It only protects you from the extra penalty.

There are separate safe harbor rules at the federal and state levels. This article focuses on California’s rules, which are stricter and more front-loaded than federal rules.

California’s Safe Harbor Rules

How much you must pay to be “safe”

In plain terms, you generally must pay enough tax during the year using one of these methods:

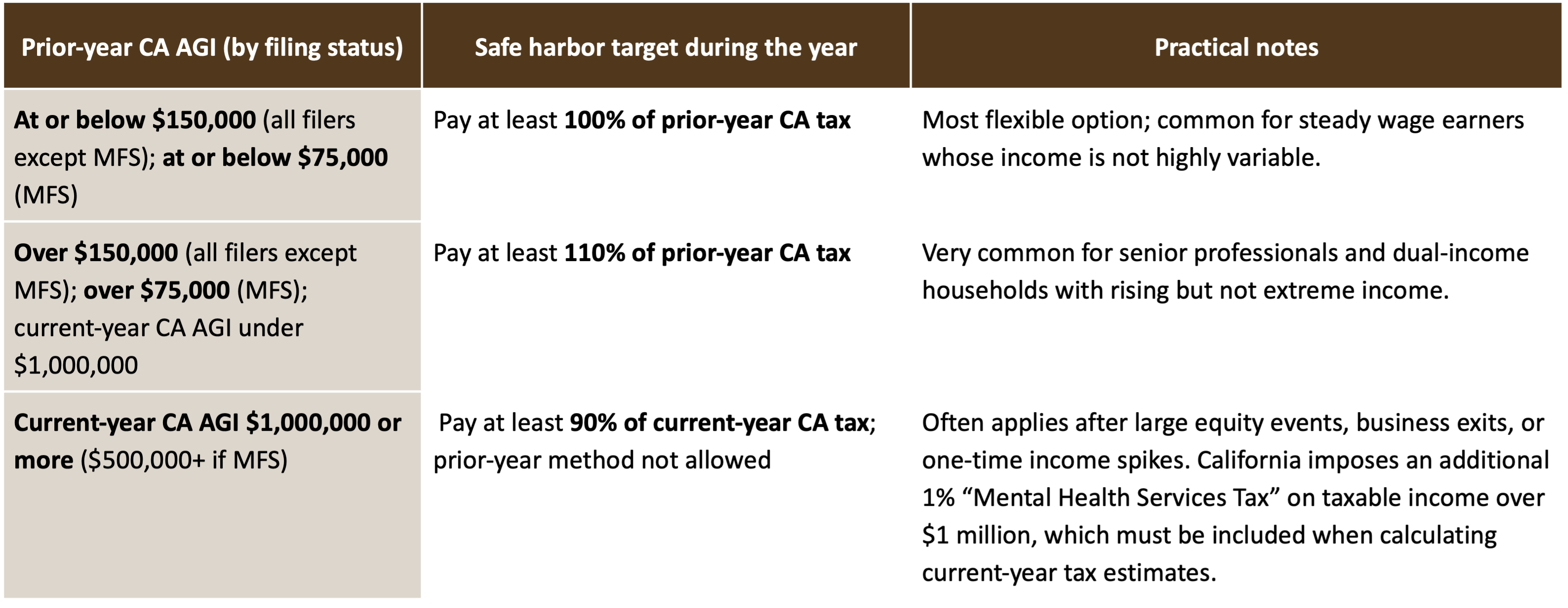

- 90% of your current-year California tax, or

- 100%–110% of your prior-year California tax, depending on income level.

“Pay” means the total of:

- California withholding (from wages, RSUs, option exercises), plus

- Timely California estimated tax payments.

As income rises, the prior-year method becomes less generous or disappears entirely.

Learn more about Summitry's equity compensation planning services.

California Individual Safe Harbor Targets (Simplified)

Exact income thresholds and percentages may change. Always confirm the current rules for the year you’re planning.

When You Must Pay: California’s Front-loaded Schedule

California doesn’t just care how much you pay, but when you pay it.

For calendar-year filers, the required annual safe harbor amount must be paid roughly as follows:

- By April: about 30% cumulatively

- By June: about 70% cumulatively

- By January (following year): 100% cumulatively

California uses a 30% / 40% / 0% / 30% installment pattern, so a third installment date exists, but no payment is due under the standard schedule.

A key trap: back-loading payments into January can still leave earlier periods underpaid, triggering penalties even if you “catch up” before filing.

Why Equity Income Makes Safe Harbor Harder to Hit

How RSUs and options create lumpy income

RSUs:

RSUs are taxed as wage income when they vest. Vesting often occurs in a few large chunks each year.

NSOs:

When you exercise non-qualified stock options, the spread between market value and strike price is wage income. A single exercise can create a massive one-time income spike.

ISOs:

Incentive stock option exercises can trigger alternative minimum tax calculations. California taxable income can rise sharply even if no shares are sold for cash.

Withholding on equity vs. actual tax owed

Employers typically use flat “supplemental” withholding rates for bonuses, RSUs, and option income. For high-income California residents, these rates are often well below the true marginal tax rate.

The result? Pay stubs may show significant tax withholding, but total withholding often falls short of the safe harbor target.

Late-year RSU vests or option exercises also tend to push AGI above the $1 million threshold, where the prior-year safe harbor disappears and required payments increase sharply.

Interaction with California’s timing rules

Timing is where equity income causes the most damage. RSUs vesting or options exercised after June make it very hard to retroactively satisfy the 30% and 70% checkpoints without proactive estimates. A large year-end equity event can create a huge current-year tax bill that still must meet the 90% of current-year tax standard for very high earners.

How Equity Holders Can Avoid Underpayment

Step 1: Map your equity events and base income

Start with a simple list:

- Base salary and expected cash bonus.

- RSU vest dates and estimated values.

- Planned NSO or ISO exercises with rough price assumptions.

A basic spreadsheet or calendar with dates and estimated taxable amounts is usually enough.

Step 2: Roughly project your California tax and safe harbor target

Use a straightforward process:

- Estimate total California taxable income.

- Apply an approximate effective tax rate or use software or professional help.

- Identify which safe harbor applies:

- Is the prior-year 100% or 110% method available?

- Will income likely cross into very-high-income territory, requiring a 90% current-year target?

- Translate this into a single dollar number, which equals your annual safe harbor amount.

Speak with a Summitry Advisor

Step 3: Compare projected tax to current withholding

Next:

- Pull year-to-date California withholding from pay stubs or payroll portals.

- Project year-end withholding if nothing changes.

Then ask:

- Am I on track to hit my safe harbor dollar target?

- Am I roughly on pace for 30% by April and 70% by June?

Step 4: Decide between higher withholding and estimated payments

Adjusting withholding

Options include:

- Updating your California withholding form to increase wage withholding.

- Requesting that payroll apply higher supplemental withholding rates to upcoming RSU vest events.

Pros:

Automatic and low-maintenance.

Cons:

Hard to fine-tune for very uneven equity income; may be overwithheld in light-equity years.

Making California estimated tax payments

Direct payments allow more precision:

- Pair payments with major RSU vests or option exercises.

- Time estimates in the same quarter as the income spike to satisfy the 30% / 70% / 100% pattern.

If large equity events are expected early in the year, calendar reminders for April and June estimates are critical.

Step 5: Revisit mid-year and before big events

Do a mid-year check after the first major vest or exercise:

- Update projected tax and withholding.

- Reassess whether income will cross high-income thresholds.

Before any large discretionary option exercise, do a quick review to decide whether an immediate estimated payment is needed.

Example: RSU-heavy employee who misses the CA June checkpoint

An employee earns a $220,000 base salary and receives RSUs that vest quarterly, with each vest worth about $200,000. Total compensation for the year is approximately $1.02 million. The employer applies California’s standard supplemental withholding to the RSU income.

By June, two RSU vests have occurred. Even though taxes are withheld from each vest and from regular paychecks, the employee has paid only about $85,000 of California tax by mid-year.

Based on projected income, the employee’s total California tax for the year will be roughly $ 285,000. Because current-year California AGI exceeds $1,000,000, the prior-year safe harbor is not available. To avoid an underpayment penalty, the employee must pay at least 90% of current-year tax, or approximately $256,500.

California’s timing rules require about 70% of that amount—roughly $180,000—to be paid by June. At that point, the employee is significantly short of the June requirement.

A large January payment brings total payments up to the safe harbor amount, but it does not fix the earlier shortfall. California assesses an underpayment penalty because the June checkpoint was missed.

*These figures are for educational purposes only

What caused the problem

- RSU income arrived in large chunks.

- Supplemental withholding on RSUs was much lower than the employee’s true tax rate.

- No tax payment was made to cover the June timing requirement.

What would have fixed it

- A targeted estimated payment made in June, tied to the second RSU vest.

- A modest increase in ongoing wage withholding for the rest of the year.

Either step, taken in time, would have satisfied both the dollar and timing rules.

California Equity Holder Safe Harbor Checklist

- Do you know your expected RSU vest dates, option exercises, and approximate dollar amounts?

- Have you estimated your total California tax and identified which safe harbor rule applies?

- Are you on track to meet both the dollar target and the 30% / 70% / 100% timing milestones?

- Have you adjusted withholding or scheduled estimates to line up with major equity events?

- Will you revisit the plan if stock prices or exercise timing change materially?

For California equity holders, safe harbor planning isn’t optional. It’s the difference between a manageable tax bill and a penalty you could have avoided with earlier, better-timed payments.

Summitry helps California taxpayers translate these rules into an actual plan, projecting income, coordinating federal and state obligations with the IRS in mind, and timing payments to help you avoid underpayment penalties. Planning ahead for equity compensation and other uneven income can help you avoid California penalties and prevent year‑end surprises.

Request a Tax Planning Consultation

This material is intended for general informational purposes only, and should not be construed as legal, tax, investment, financial, or other advice. It does not consider the specific investment objectives, tax and financial condition or needs of any specific person. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Investing involves the risk of loss, including loss of principal.

GET THE NEXT SUMMITRY POST IN YOUR INBOX: