Schedule a talk with one of our advisors to learn more about Summitry and how we can help you get a foothold on your financial life. For career opportunities please visit careers at Summitry.

Team

Insights

Pages

- Let's Talk

- Phone / Directions

How to Calculate, Plan, and Minimize the Alternative Minimum Tax (AMT) on Your Incentive Stock Options

Summitry

Aug 27, 2025

The Alternative Minimum Tax (AMT) is a parallel tax system designed to ensure that taxpayers who benefit from certain deductions and credits still pay a minimum level of tax. While AMT can affect many high-income taxpayers, it is a common consideration for those who exercise Incentive Stock Options (ISOs).

When you exercise ISOs, the “bargain element” — the difference between the option’s strike price and the fair market value at exercise — is treated as income for AMT purposes (not for regular tax purposes), even if you haven’t sold the shares yet. This can cause you to owe AMT in the exercise year.

The good news: For ISOs, this AMT is often a timing issue rather than a permanent higher tax. Paying AMT from an ISO exercise typically generates a dollar-for-dollar AMT credit you can use in future years when your regular tax exceeds AMT, often when you sell the stock. Over time, this credit helps you “make up” the initial AMT paid, effectively turning it into a temporary prepayment instead of an extra long-term tax.

What is the AMT and Why Does It Exist?

The AMT is a “backup” tax system. Each year, you must calculate your taxes twice — once under regular rules and once under AMT rules — and pay whichever is higher. AMT was introduced in 1969 to prevent high-income earners from using deductions and credits to eliminate all federal tax liability.

Think of the AMT as a floor that your tax liability can’t fall below. If your deductions and credits push your regular tax below the AMT threshold, AMT ensures you still pay a minimum amount. While certain AMT triggers can result in a permanent higher tax (with no credit recovery), ISO-related AMT usually is only temporary due to the AMT credit mechanism.

Paying AMT isn’t necessarily a bad thing, depending on your financial situation. It’s a good idea to speak with a financial advisor or tax specialist before exercising to determine the optimal time to exercise or sell.

Understanding ISOs and AMT

ISOs are a type of employee stock option that gives you the right to buy company shares at a fixed “strike” price — often below market value — as part of your compensation, particularly in startups and fast-growing companies.

Their appeal lies in favorable tax treatment: you don’t pay ordinary income tax when exercising, only when selling, and if you hold the shares at least one year after exercise and two years after grant, your gains qualify for long-term capital gains rates. However, the IRS counts the difference between the strike price and market value at exercise (the “spread”) as income for AMT purposes, creating “phantom income” that can result in a significant AMT bill if the spread is substantial.

Who is Subject to the AMT?

Not everyone pays the AMT. It mostly affects:

- High-income taxpayers with large deductions or credits.

- People who exercise ISOs.

- Taxpayers with large capital gains.

- Taxpayers who have income from tax-exempt private activity bonds.

If your income is below certain thresholds–about $88,100 for singles or $137,000 for married filing jointly in 2025–you’re unlikely to owe AMT. But if you’re near or above those thresholds, it’s important to understand how AMT might impact you.

Impact of the Tax Cuts and Jobs Act (TCJA) on AMT

The TCJA, in effect from 2018 to 2025, made AMT far less common by:

- Significantly increasing exemption amounts.

- Raising phase-out thresholds.

- Limiting or eliminating many deductions that previously triggered AMT.

These provisions were set to expire after 2025, but the One Big Beautiful Bill (OBBB), enacted in 2025, made them permanent. By locking in the higher exemptions and thresholds, OBBB prevents a reversion to much lower pre-TCJA levels, keeping many taxpayers, especially those with ISOs, out of AMT.

The OBBB resets the inflation adjustment base year from 2017 to 2025, slightly slowing future growth in exemptions, but the amounts remain far above pre-TCJA levels. These changes will continue to be adjusted annually for inflation and provide ongoing relief for taxpayers with ISOs, large capital gains, or significant state and local tax deductions.

Taxpayers and financial advisors should prepare for these changes, possibly adjusting tax planning strategies accordingly.

How is the AMT Calculated?

Calculating AMT is complicated, but here’s a simplified step-by-step overview:

- Calculate your regular taxable income as reported on IRS Form 1040.

- Adjust your income for AMT purposes by adding back disallowed tax preferences and deductions. For example:

- State and local tax deductions (SALT).

- The standard deduction if you claim it.

- Tax-exempt interest from private activity bonds.

- Certain depreciation related to rental real estate.

- Investment income or deductions from partnerships that require AMT recalculation.

- Other potential adjustments may apply, depending on your individual situation.

- The result is your Alternative Minimum Taxable Income (AMTI).

- Subtract the AMT exemption amount (if eligible) from your AMTI.

- For 2025, the exemption amounts are:

- $88,100 for single filers

- $137,000 for married filing jointly

- $68,500 for married filing separately

- For 2025, the exemption amounts are:

- Apply AMT tax rates to the remaining income:

- 26% on AMTI up to $239,100 (for most taxpayers)

- 28% on AMTI above $239,100

- Subtract any AMT foreign tax credit if applicable.

- Compare the AMT liability to your regular tax liability and pay the higher amount.

- Special note for ISO exercises: If your AMT liability is higher because of an ISO exercise, the extra AMT paid often generates a dollar-for-dollar AMT credit you can carry forward to future years when your regular tax exceeds AMT (often the year you sell the ISO shares). This makes AMT for ISOs generally a timing issue rather than a permanent extra tax — unlike some other AMT triggers that offer no such credit.

- This process is done using IRS Form 6251.

These amounts reflect the most recent tax law (2025), and exemption amounts may change in future years.

Because AMT adjustments and thresholds can change and may impact taxpayers differently with the 2025 SALT cap increase to $40,000, consult updated IRS guidance or a tax professional for your specific situation. For the full adjustment list and calculation method, see the IRS Form 6251 instructions.

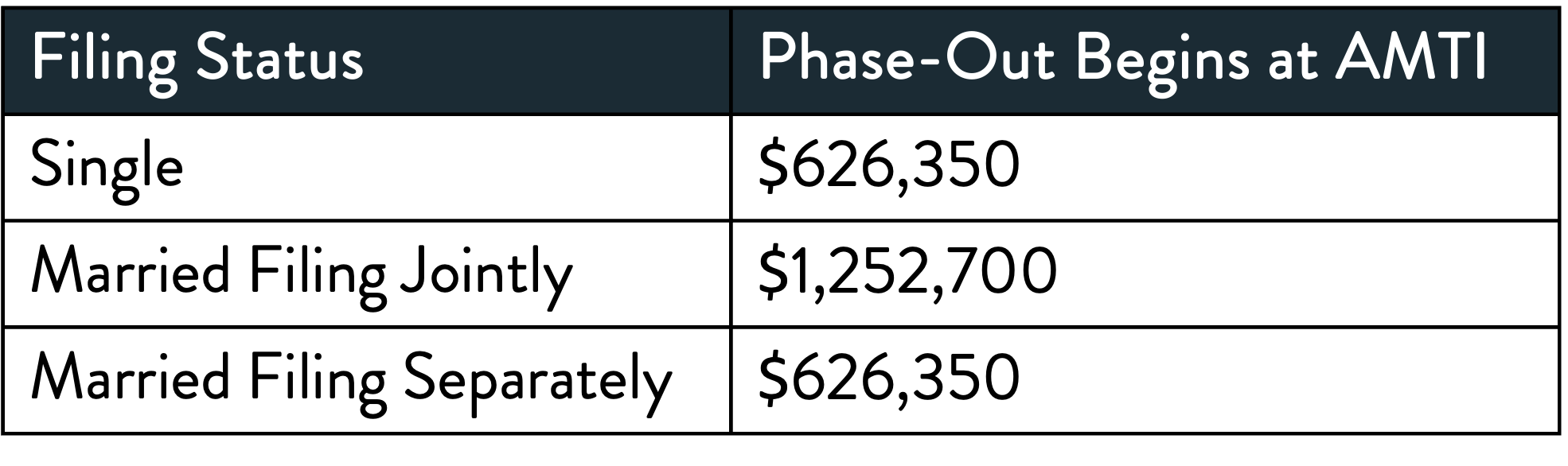

AMT Exemption Phase-Outs

The AMT exemption isn’t a fixed amount for everyone. It phases out for higher-income taxpayers, meaning the exemption amount decreases by 25 cents for every dollar of AMTI above certain thresholds.

For 2025, the phase-out thresholds are: Once your AMTI exceeds these amounts, your exemption shrinks, increasing your AMT liability. This phase-out can cause taxpayers in certain income ranges to face an effective marginal tax rate higher than the regular rates.

Once your AMTI exceeds these amounts, your exemption shrinks, increasing your AMT liability. This phase-out can cause taxpayers in certain income ranges to face an effective marginal tax rate higher than the regular rates.

AMT Tax Rates and Brackets

The AMT uses two tax rates: These rates are generally higher than the regular tax rates for some income levels, which is why AMT can increase your tax bill.

These rates are generally higher than the regular tax rates for some income levels, which is why AMT can increase your tax bill.

How Can You Manage or Minimize AMT Liability?

While AMT can’t be avoided entirely if you meet the criteria, there are planning strategies to reduce its impact:

- Timing Income and Deductions: Accelerate or defer income and deductions to avoid AMT in a particular year.

- Exercise Stock Options Carefully: Plan ISO exercises to minimize AMT exposure, possibly spreading exercises over multiple years.

- Manage Capital Gains: Consider timing sales of appreciated assets.

- Use AMT Credits: AMT credits from ISO exercises are carried forward indefinitely and offset regular tax (not AMT) in future years. This credit feature often means ISO-related AMT is temporary, and you can recover the tax over time.

SPEAK TO A FINANCIAL ADVISOR

Frequently Asked Questions

Q: Can AMT credits be carried forward?

Yes. If you pay AMT due to certain deferral items (like ISO exercises), you can claim an AMT credit in future years when your regular tax exceeds AMT.

Q: Does AMT affect state taxes?

Some states have their own alternative minimum tax (AMT) rules, while many others do not. It’s important to review your specific state tax regulations to understand how AMT may apply. For example, as of 2025, California imposes a flat AMT rate of 7%.

Q: Can AMT cause me to owe tax even if I have no regular tax liability?

Yes. AMT ensures a minimum tax liability, so even if your regular tax is zero, you may owe AMT.

Q: At what income level does AMT kick in?

The AMT generally kicks in when your AMTI exceeds the exemption amounts for your filing status. For 2025, these exemptions are about $88,100 for single filers and $137,000 for married filing jointly.

Q: Who is subject to AMT?

Taxpayers subject to AMT are typically those with higher incomes who also claim certain deductions or have income types that the AMT system treats differently. Common triggers include:

- Exercising incentive stock options (ISOs)

- Having large capital gains

- Claiming significant state and local tax deductions (which AMT disallows)

- Taking tax-exempt interest from private activity bonds

Do You Have an AMT Action Plan?

Understanding how AMT works, what triggers it, and how to plan for it can save you from unexpected tax bills and help you make smarter financial decisions. If you think you might be subject to AMT, consider consulting a tax professional. It’s not a tax to fear, but one to respect and plan around.

At Summitry, we don’t view tax planning in isolation. We integrate it seamlessly into your overall wealth management, investment strategy, and financial plan. For high-net-worth individuals and those with complex equity compensation like ISOs, we craft personalized strategies that minimize AMT exposure while aligning with your long-term financial goals. By considering taxes alongside investing, estate planning, and cash flow management, we help you make smarter, more holistic decisions that protect and grow your wealth over time.

SPEAK TO A SPECIALIST

GET THE NEXT SUMMITRY POST IN YOUR INBOX:

MORE INSIGHTS AND RESOURCES

Let's talk

Schedule a talk with one of our advisors to learn more about Summitry and how we can help you chart a path for your financial future.

Alex Katz

President